Having bad credit can set you up for a multitude of challenges, from loan approval to a renter’s agreement on your apartment. Credit score is a three-digit numeric number found in the Credit Information Report and it plays an integral role in initiating the loan application process. The lower the score, the more trouble you may face. In case, you have bad credit history, it is necessary to follow certain measures to fix the issue. Credit repair is a way to improve score without paying one penny further.

Do you have a remarkable Credit Card balance? Try not to stress; we’ve all been there. A free credit report is typically the initial step when you’re new to the interaction. You’ll need to comprehend the intricate details of credit reports, particularly if your credit score rating needs a lift.

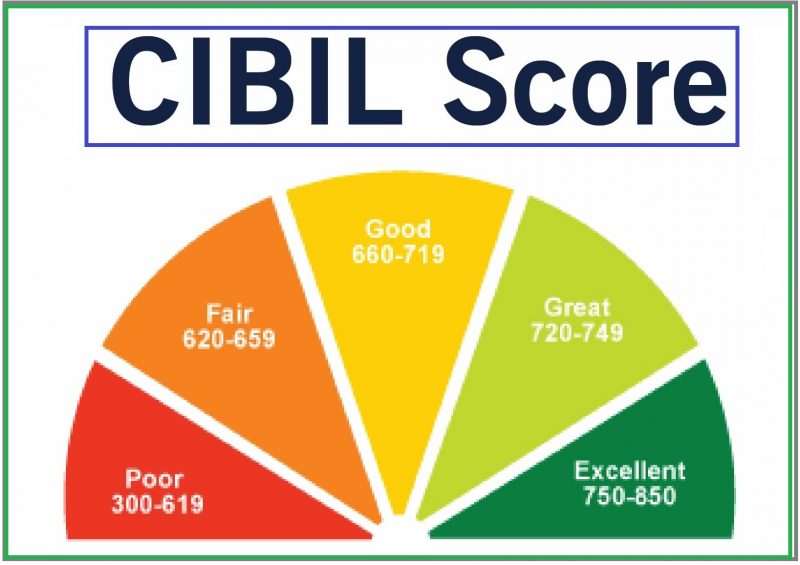

1. Check CIBIL Score Report at Regular Intervals

After availing the credit score report, check the number of open records there are against your name. In this segment, you may deal with two issues like the notice of records not opened by you, and the record has been shut by the bank. On the off chance that CIBIL has made a question, you can contact the loan specialist for finding the cure rapidly. Notwithstanding the specific situation, the report contains the record name, account type, account number, and possession data. The record subtleties are additionally referenced including credit limit, current equilibrium, endorsed sum, reimbursement residency, sum late, EMI sum, money breaking point, and installment recurrence.

2. Dispute Negative Marks

In the old days, you had to write letters to the credit bureaus if you wanted to dispute errors. Now services like Credit Karma let you dispute errors online.

Start with derogatory marks like collection accounts and judgments. It’s not uncommon to have at least one collection account appear on your report. I had two from health care providers I used after having a heart attack; my insurance company kept claiming it had paid while the providers said it had not, and eventually the accounts ended up with a collection agency. Eventually I decided to pay the providers and argue with the insurance company later, but both collections wound up on my credit report.

Fixing those problems was easy. I clicked the “Dispute” button, selected “The creditor agreed to remove my liability on this account,” and within a week the dispute was resolved and the entry was removed from my credit report.

You can also dispute errors through each credit bureau. If that’s your preference, go here for TransUnion, here for Equifax, and here for Experian. Keep in mind some disputes will take longer than others. But that’s OK. Once you initiate a dispute, you’re done: The credit bureaus are required to investigate it and report the resolution. Spend as much time as it takes trying to have derogatory marks removed because they also weigh heavily on your overall score.

3. Plan your Credit

Many people whose scores fall drastically are ones who do not plan their finances well. If you apply for too many credit cards just to increase your credit limit, but are unable to pay the bills off on time of all of them, then you will be left with a huge outstanding balance and history of delayed payments that will decrease your score by a lot. Also, applying for unplanned loans can leave you in a very bad financial state, if you are not able to repay them. Thus, it is important to plan credit and apply for a credit card/loan only if it is absolutely required and when you are sure that you will be able to repay the amount you borrow.

Credit score cannot be repaired in a day or two. It requires time, patience and planning. Once your credit score improves, try to not make any mistakes that will harm it. If you do not have a credit score at all, then try to build it by applying for a regular or secured credit card.

4. Monitor the Payment History and take action

Check the past due section of each account and anything besides, ‘XXX’ and ‘000’ are considered in a negative context. You should pay EMIs and bills on time, as when you miss payments, it brings the score down. Also, take a look at the ‘settled’ or ‘written off’ account because it is considered in a negative light. You can raise your concern with CIBIL if the account is tagged in a wrong way. You can start to resolve the issue by contacting CIBIL and the authority will respond to your query within 30 days. However, if the respective financial institution confirms the transactional information to be true, CIBIL cannot make any changes. In this case, it is better to be in touch with the bank for expediting the procedure directly.

5. Pay on Time

Even one late payment can hurt your score. Do everything you can, from this day on, to always pay your bills on time. And if one month you aren’t able to pay everything on time, be smart about which bills you pay late. Your mortgage lender or credit card provider will definitely report a late payment to the credit bureaus, but utilities and cell providers likely will not.

Check the “Accounts” section on your credit reports to see which accounts are listed, and if you have to pay late, choose an account that does not appear on your report. Then work really hard to make sure you can always pay everything on time in the future. Your credit score will thank you, and so will your stress levels.

6. Prepayments

In past, you might have had prepaid loans. At that time, the thought of fixing credit score and bettering it must have also occurred. However, the early payments never repair credit score. The only thing you should keep in mind is to make timely payments for keeping up a steady history.

7. Increase Your Credit Card Limit

Higher credit scores are often due to maximum limits on credit cards, indicating that an individual is responsible enough to handle that specific amount. If you’re not confident in your ability to handle your finances just yet, avoid this route. You could end up in a worse place, and that added stress isn’t worth it.