What creates a good CIBIL Score?

CIBIL, which is the most common credit bureau, puts anyone with little credit history and people with a very high risk of default in the range of 300 credit score. However, there are chances your score may be less than 300 when you have no credit history. In this case, you may want to build one.

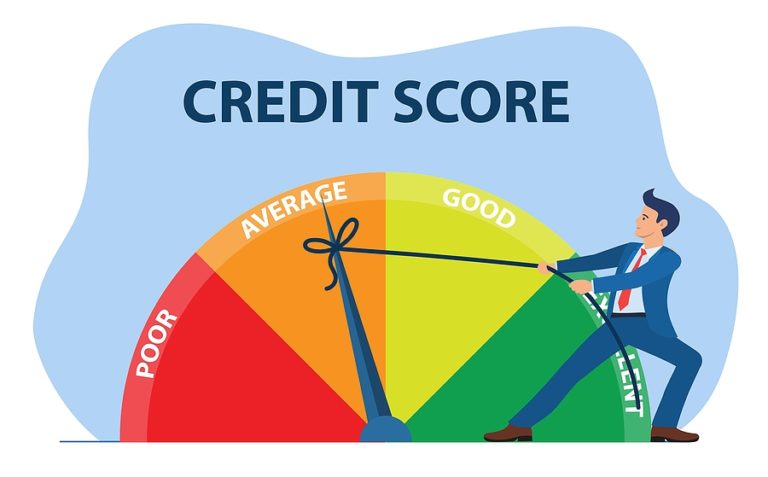

Anything between 400 when your credit score is between 600, you are considered moderately risky. The chances of getting a loan are low, but the terms of lending would not be very favourable to you.

If you are within the 700-750 score, your credit record is satisfactory and you will probably get a loan at competitive rates when compared to scores below. CIBIL says about 10% of all the new loans sanctioned fall within this band.

Credit scores of 750-799 are considered good and you will generally face very little difficulty in raising a loan. However, do keep in mind that credit score is not the only deciding factor in the disbursement of a loan, but one of the important ones. Finally, any credit score above 800 is considered excellent and Is generally reflective of someone with good control over his or her finances and a proven track record of clearing the dues. Lenders would rarely hesitate in lending to this class of borrowers.

There are other credit rating agencies like Experian that have a similar score range of 300-900 points, with 300 being the lowest and 900 being the highest. Equifax on the other hand scores individuals on a scale of 1 to 999, with 1 being the lowest and 999 being the highest. While each credit agency has its own formula and algorithm to reach your credit score, you would get an idea about where you stand if you get the score from just one agency.

How to get a Bad-Credit Personal loan?

Getting a personal loan with bad credit isn’t impossible, but it requires diligent research to find the most affordable loan possible. Here are a few steps to get a personal loan if you don’t have strong credit.

- Check your credit score: Learn where your credit stands by requesting a free credit report from com. You are entitled to one free credit report every year from each of the credit reporting agencies, though you can currently access weekly reports through April 2022.

- Ensure that you can repay the loan: Evaluate your home budget to make sure that you can support an additional monthly loan payment.

- Compare bad-credit personal loans: If you have an existing relationship with a bank or credit union and your accounts are in good standing, it may have a personal loan option for you. You can also research personal loans for people with bad credit online, but make sure to read the fine print and independent reviews about the lender.

- Take advantage of prequalification: Before you apply for a loan, many online lenders allow you to prequalify, or check whether or not you will qualify without doing a hard credit check. This is a good way to shop around for a bad credit loan without impacting your credit score further.

- Look into secured loans: Some lenders offer secured personal loans, which are often easier to get if you have below-average credit. These loans must be backed by an asset like your home or car, but they typically have lower APRs.

- Add a co-signer if necessary: Co-signers take on partial responsibility for the loan and may be required to repay the loan if they fall behind on payments. Adding a co-signer who has good credit could help you qualify and may net you lower interest rates.

- Gather financial documents: When applying for a loan, you’ll likely have to provide financial documents that include pay stubs, tax documents, and employment information. By gathering all of these documents in advance, you’ll speed up the process of acquiring your loan.

- Be prepared for a hard credit check: While you can get prequalified from many lenders without initiating a hard credit check, the actual application will result in a credit inquiry. A hard credit check can temporarily damage your credit, though you should be able to recover the points lost once you begin making payments on the loan.

What makes up a Bad Credit Score?

FICO calculates your credit score using five pieces of information:

- Payment history: 35%

- Amounts owed: 30%

- Length of credit history: 15%

- New credit: 10%

- Credit mix: 10%

If your finances fall short in one or more of these areas, your score will drop. For instance, having a history of late payments will have a huge impact on your score, since payment history contributes the most to your score. Things like bankruptcies, foreclosures, and high amounts of debt relative to your income could also result in a bad credit score.

How to improve your CIBIL Score?

If you happen to have a CIBIL score that is not good, then there is no reason to lose heart. There are things you can do to improve that score. Here are some tips that can help you improve your credit rating.

- If you have credit cards with outstanding balances then you need to pay them back at the earliest possible because even if you pay the minimum due, it only gets the bank off your back, the remaining is still considered outstanding by CIBIL.

- If your credit score is not good, try to keep the borrowing down to a minimum. Doing this will give you time to recover from your current debt without creating new debt.

- Let’s assume that you have cleared all your debt and decide that to celebrate your freedom from the debt you will cancel all your credit cards, DON’T! If you cancel all your cards, then you won’t be able to create a credit history when you need one at a later stage.

- If you don’t have cards or loans that can help you create a credit history to get your score going, you can always go in for a secured loan like a vehicle loan. Sure you may not get the best interest rate on such a loan but at least you may get a loan that can help you jump start your credit history.

- There are times when you move into a house and realise that because of the misdeeds of the person who stayed there before you, the address has been blacklisted. What you can do in this case is to inform CIBIL of the mistake and get it corrected.

- As far as using your credit cards are concerned, make sure you don’t come close to the limits of your cards too often. If you do, then your score might deteriorate further.

- In case you can’t get a loan or a credit card to get the history going what you can do is to approach banks that provide credit cards against fixed deposits (FDs). The idea is that you open an FD with them and they will issue you a credit card that has a limit slightly lesser than your FD amount. This will get you into the credit system and get your credit history going.

- In time, even utility bill payments are going to affect your CIBIL score so it’s best to make a habit of making sure that ALL your bills are paid in full and on time.

- If you are rejected for a loan or credit card once, don’t keep applying for one at other banks. Take some time out to fix your score and then apply again.

What is considered a Good Credit Score?

Categories of Credit Score:

Payment history (35% of score): Do you pay your bills on time, every month?

Amounts owed (30%): How much do you owe on your credit accounts, particularly relative to your credit limits or original loan balances?

Length of credit history (15%): This considers various time-related factors, such as the age of your individual accounts, the age of your oldest account, and the average age of all of your accounts.

New credit (10%): Newly opened credit accounts, as well as your recent applications for credit, are included in this category.

Credit mix (10%): Lenders want to see that you can be responsible with different types of credit, so having several different types of accounts (credit card, mortgage, auto loan, and so on) can boost your score.